Dr Copper risk becoming noise, not a signal

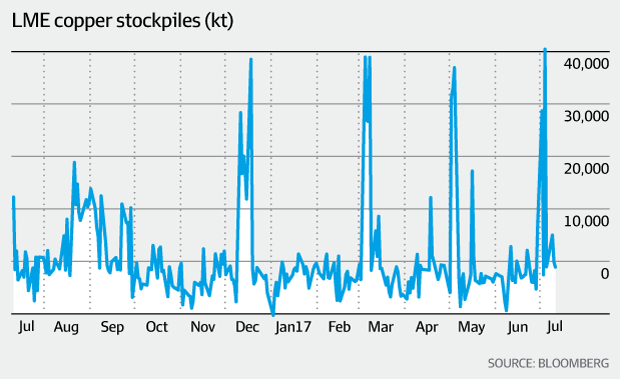

Stocks of copper registered with the London Metal Exchange (LME) jumped by a net 72,625 tonnes, or 30 per cent, in the space of just four days starting June 29.

That was courtesy of whoever warranted 86,950 tonnes of metal in LME sheds.

It was the fourth time since December that LME copper stocks have been rocked by huge inflows. All four "arrivals events" have been unprecedented in scale, and the cumulative inflow has been in excess of 500,000 tonnes.

Stocks of copper have surged in recent weeks, distorting the picture of supply and demand in the market. Bloomberg

The London aluminium market has grown accustomed to huge tonnages appearing and disappearing in the LME warehouse network.

But prior to last December the largest concentrated warranting in the copper market took place in February 2015, when 32,750 tonnes showed up on a single day.

These running stock shocks have obscured any coherent market narrative behind a lot of smoke and several mirrors.

Copper is a market that is collectively trying to work out whether it is in supply surplus or shortfall. Opinions are divided. The median forecast in the latest quarterly Reuters base metals poll of analysts was for a 17,000-tonne deficit for 2017.

Well, good luck trying to discern such a small market balance from LME stocks right now.

Don't despair, however.

There's a bigger stocks picture which is generating a better signal of copper's supply-chain dynamics. It's just that the LME's part in that picture appears to be changing.

Merry-go-round

This latest "arrivals event" is just another whirl of a copper stocks merry-go-round that has been spinning for many months.

The previous three spins took place in May, March and last December. There was a precedent in August 2016 as well, although the warranting action in that month was more dispersed.

There are two common themes to all these stocks shocks.

What enters the system does so primarily at Asian locations. Cumulative "arrivals event" inflows have been concentrated on the ports of Busan in South Korea, Singapore, Kaohsiung in Taiwan and Port Klang in Malaysia. The only exception has been Rotterdam, which has seen significant inflows over the same days.

And what enters the system doesn't stay around for long.

May's "arrivals event" saw 126,150 tonnes warranted in just three days, boosting headline stocks to a six-month high of 354,650 tonnes. By the time of the most recent surge, however, they had fallen back to 243,300 tonnes.

What's going on?

A big bull-bear battle is what's going on.

One rooted in physical flow, warehousing and arbitrage dynamics. Metal is being relentlessly shuffled between LME and off-market storage and between geographic locations.

Reading the game is hard because most of it is taking place in the physical market shadows.

This feud has also become a battle of market narrative, each player using LME stocks to express an opposing view.

The problem is that the smoke of battle has hopelessly distorted any stocks' pricing signal, bullish or bearish. An LME copper stocks chart right now looks like a badly drawn zig-zag.

And it's getting worse, because this merry-go-round seems to be turning ever faster.

The bigger picture

There is some good news, though.

Firstly, it's questionable just how much these games with LME stocks have impacted price.

LME three-month copper has held station in a broad $US5420-6205 a tonne range since the start of December.

Time-spreads, which should be more sensitive to stocks shocks, have largely held steady over the same period. The benchmark cash-to-three months spread

Secondly, LME stocks are only one third of the visible copper stocks picture. The other two components are the Shanghai Futures Exchange (ShFE) and CME (COMEX).

Taking all three together, as of last Friday the cumulative net change so far this year was a build of 114,040 tonnes.

It's not an outlandish signal, factoring in both this year's increased scrap availability and lower Chinese imports.

Nor is it dramatically out of line with the latest market balance assessment from the International Copper Study Group. According to the ICSG, the global refined market recorded a supply surplus of 164,000 tonnes or, seasonally adjusted, 72,000 tonnes in the first quarter of this year.

Mitigating volatility

The bigger picture is clearer because the other two components have acted in different ways to mitigate the volatility emanating from the LME stocks battleground.

First, ShFE stocks have tended to move inversely to those registered with the LME.

The net stocks change across the two exchanges over the first half of 2017 was a decline of just 3528 tonnes.

This is not coincidental since China sits at the centre of the Asian physical and arbitrage markets, placing it at the heart of the ongoing tug-of-war between bull and bear. ShFE stocks have become a second, more distant front in the same struggle.

Second, without anyone paying too much intention, COMEX warehouses are filling up to levels not seen in many, many years.

Total deliverable stocks currently stand at 164,184 imperial tons, equivalent to 148,947 tonnes, of which all but 1447 tons are on warrant. It's the highest count since May 2004.

Even with the latest "arrivals event" in the LME system, it is the 68,026-tonne rise in COMEX stocks that has generated most of the global exchange stocks increase this year.

Realigning the lens

The COMEX warehouse system has only US good delivery points so should, in theory, be largely reflective of domestic market availability.

But this stocks build has been running for 11 straight months and suggests something more structural than cyclical.

It's possible we're seeing a reaction to the threat of US trade tariffs. The prospect has caused a shift in physical market flows in several industrial metals as merchants look to build "just in case" inventory in the United States.

It's also possible that rising exchange inventories are in some way related to rising trade activity on the CME copper contract, although disentangling cause and effect is an impossible task.

CME copper volumes rose by 18.5 per cent in the first seven months of this year and, equally significantly, open interest at the end of June was up by 59 per cent.

It's all part of an increasingly complex global trading environment for old "Dr Copper". Trading is no longer concentrated just on the LME but is dispersing in still-evolving ways across all three major time zones.

Copper stocks may be starting to mirror that new landscape.

Certainly, the COMEX warehouse system is no longer a marginal part of the global stocks picture. COMEX copper stocks currently account for 23 per cent of global exchange stocks.

They have been the key driver of the overall rise in visible inventory this year, a trend that has been lost in the noise of the LME system and the echo from the ShFE system.

So, if you're finding LME stocks a bit of a confusing read right now, take a step out of the optical illusion machine and focus on the bigger picture.

Reuters

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Commodities

Fetching latest articles